Wise vs. Revolut in 2026: An Analytical Audit of Liquidity Risks and Compliance Layers

The Illusion of Frictionless Outflows

In the mid-2026 financial climate, the primary concern for a strategic investor is no longer the “sleek interface” it is Liquidity Survival. As global financial hubs activate high-velocity surveillance protocols, the dream of spending crypto profits abroad has hit a wall of algorithmic freezes.

This liquidity friction is not an isolated event but a direct symptom of the ongoing Liquidity War between Neobanks and Traditional Giants. As established institutions tighten their grip on capital outflows, fintech nodes like Wise and Revolut are being forced to act as the first line of regulatory defense.

While retail users still compare Wise and Revolut based on card colors or weekend FX markups, a surgical audit reveals a darker reality. These platforms are no longer just “apps”; they are high-compliance nodes. Choosing the wrong one in 2026 means risking a 90-day capital lock while your funds sit in “compliance limbo.”

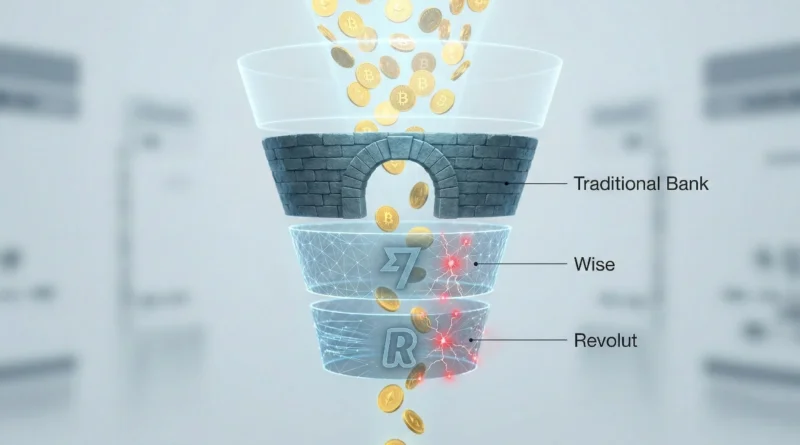

1. Wise: The “Fiat Purist” and the Source-of-Wealth Wall

Wise has doubled down on its identity as a transparent fiat rail. However, its hostility toward non-institutional crypto flows is now a systemic risk for the user.

- The Acceptable Use Trap: In 2026, Wise remains fundamentally “anti-crypto” for P2P or unverified exchange flows. Their algorithms flag incoming transfers from offshore or decentralized platforms as high-risk events.

- The 21-Day Latency: Sending fiat converted from a DEX directly to Wise triggers a Source of Wealth (SOW) audit. Their compliance checks can freeze a “digital nomad” account for weeks, demanding forensic proof of every on-chain move.

- The Verdict: Wise is a precision tool for moving audited fiat. It is a dangerous choice for those attempting to off-ramp “grey-market” profits.

2. Revolut: The Surveillance Premium

Unlike Wise, Revolut allows direct asset liquidation, but this “convenience” is a trade-off for total transparency.

- Automated Fiscal Sync: By 2026, Revolut’s internal exchange is fully integrated with national tax engines. Every “Sell” click triggers a real-time data packet to authorities. You are not “spending crypto”; you are liquidating assets in a fishbowl.

- The Shadow Spread: While advertising “low fees,” the hidden spread inside the app often deviates 1.5% to 2.5% from the actual spot price. You are paying a “Stealth Tax” for the privilege of instant liquidity.

While we have previously analyzed how this platform serves as a primary Bridge between Traditional Banking and Web3, the 2026 reality is that this bridge now functions as a one-way data funnel. For the high-net-worth investor, the convenience of a “super-app” must be weighed against the risk of total fiscal exposure.

3. Execution Audit: 2026 Risk Matrix

| Risk Vector (2026) | Wise (Fiat Specialist) | Revolut (Integrated Hub) |

| Crypto On-Ramp | Restricted (External only) | Native (Surveilled) |

| Tax Reporting | Indirect / Bank-led | Real-time / Automated |

| AML Sensitivity | Extremely High (External) | Behavioral (Internal) |

| Exit Speed | 1-3 Business Days | Instant (Ledger move) |

4. Forensic Off-Ramping: The “Buffer” Strategy

To prevent a permanent account ban in 2026, follow the Audit-First protocol:

- The Intermediary Layer: Never send funds directly from a private wallet to Wise or Revolut. Use a Tier-1 Regulated CEX as a buffer.

- The Ownership Rule: Under current EBA guidelines, be ready to prove ownership of any wallet that has touched these apps.

- Low-Velocity Movement: Do not off-ramp your entire travel budget at once. Move 15-20% every 14 days to avoid triggering “Automated Account Restrictions.”

5. The Geopolitical Compliance Gap: A Border-Control Reality

In 2026, the most dangerous moment for a crypto-funded traveler is the Cross-Border Liquidity Gap. Both Wise and Revolut operate under the “Perpetual KYC” (pKYC) standard, but their execution triggers differ based on your physical location.

- The Zero-Threshold Trap (EU & UK): Within the European Economic Area, the Travel Rule is now fully operational with a zero-threshold policy. Every single transaction—no matter how small—carries a full data packet of your identity. If your Revolut account was funded via an unverified DEX three months ago, the pKYC systems are likely to trigger a Point-of-Sale (POS) decline followed by a request for a live video verification the moment you try to use the card in a new jurisdiction.

- The “Grey-List” Quarantine: Wise is particularly sensitive to IP address changes combined with crypto-origin fiat. Logging into your Wise app from a “Grey-Listed” jurisdiction and attempting a large transfer to a local bank will often park the funds in a “Review Status.” In 2026, being “under review” is functionally equivalent to being hacked: you have zero access to your capital while the compliance clock ticks (typically 60 to 90 days for complex audits).

6. Forensic Off-Ramping: The “Buffer” Protocol

To prevent a permanent account ban in 2026, you cannot simply “send and hope.” You must follow an Audit-First protocol before your capital touches a fintech interface.

- The Intermediary “Cleansing” Layer: Never send funds directly from a self-hosted wallet (cold storage) to Wise or Revolut. Use a Tier-1 Regulated Exchange (CEX) as a buffer. These entities are now required to provide the “Travel Rule Packet” that Wise requires to accept the deposit.

- The Ownership Mandate: Under the latest EBA (European Banking Authority) guidelines, any transfer exceeding €1,000 from a private wallet to a regulated platform requires proof of ownership (e.g., message signing). Keep your wallet signatures ready; the platform will ask for them the moment that fiat hits your account.

- Low-Velocity Execution: Do not off-ramp your entire travel budget in a single transaction. Use a “Low-Velocity” strategy: move 15–20% of your required liquidity every 14 days. High-velocity inflows followed by immediate international spending are the primary triggers for Revolut’s “Automated Account Restriction” algorithms.

7. The Layered Exit Strategy: Professional Flow Management

In 2026, a strategic investor does not “store” wealth in fintech; they flow it. Instead of a static balance, you must manage your capital through a Three-Layer Friction Filter:

- Layer 1: The Sovereign Buffer: This is your “clean room.” Keeping your core wealth in a Tier-1 bank is essential to shield it from the contagion risks found in newer financial instruments. As evidenced in our recent audit on Restaking and the Systemic Risks of Ethereum, chasing yield through shared security protocols can often compromise the very liquidity you are trying to protect.

- Layer 2: The High-Velocity Filter (Wise): Move only the specific amount needed for major international payments (rent, taxes, large purchases). Wise acts as your Forensic Bridge because its mid-market rates are unmatched for transparent, large-scale transfers.

- Layer 3: The “Burner” Wallet (Revolut): Use Revolut as a tactical tool for daily spending and “Last-Mile” liquidity. Keep only 7–10 days of operational cash here. If an algorithm triggers a “behavioral freeze” on your Revolut card while you are at a restaurant in Tokyo, your Layer 1 and Layer 2 capital remains untouched and accessible via other rails.

Final Audit: The 2026 Verdict

In 2026, interest rates and travel perks are mere distractions. The real cost of using these platforms is the Surveillance Premium.

- Wise is for the Transparent Auditor: Best used for pre-planned, large-scale fiat movements where documentation is ready and execution cost is the priority.

- Revolut is for the Tactical Spender: Best used as a “hot” interface for instant, low-value transactions, provided you accept the “Closed-Loop” surveillance of your spendable balance.

Conclusion: In a high-velocity market, being “insured” but “frozen” is equivalent to a 100% loss. Diversify your interfaces not just your assets to ensure you are never at the mercy of a single compliance algorithm.